Shovit Goyal, a Financial Content Creator who has spent 6 years teaching professionals how to turn their spending into savings.

Key Takeaways

Here is the main idea of the article

- Cashback is Real Money: A cashback credit card pays you back a small part of the money (usually 1% to 5%) every time you spend.

- The 80/20 Secret: Most people (80%) spend most of their money on just a few things. For young professionals, this is Online Shopping (like Amazon, Flipkart) and Food/Bills (like Swiggy, Zomato, GPay).

- Pick a Card That Fits: The best card for you is the one that gives the highest cashback on your biggest spends. Don’t get a fuel card if you don’t drive.

- Our Top 3 Picks: Based on this 80/20 rule, our top picks for most people are the Cashback SBI Card, HDFC Millennia, and Axis Bank ACE.

- Watch for Traps: Always check for two things: the Annual Fee (the cost of the card) and the Cashback Cap (the maximum cashback you can earn per month).

Getting Paid to Spend: A Simple Guide to Cashback Cards

What if you got a small refund every time you bought groceries, paid a bill, or ordered food?

That’s exactly what a cashback credit card does. It’s a simple tool. When you buy something, the bank gives you a small percentage of that money back.

But there is a problem.

Banks have hundreds of cards. Some promise 10% cashback, but only at one store. Others promise rewards, but the rewards are hard to use. It’s confusing. Many people get the wrong card and end up saving very little.

This article will fix that. We will use a simple rule to find the best card for you.

Why You Must Choose the Right Card

Choosing the right cashback card is very important.

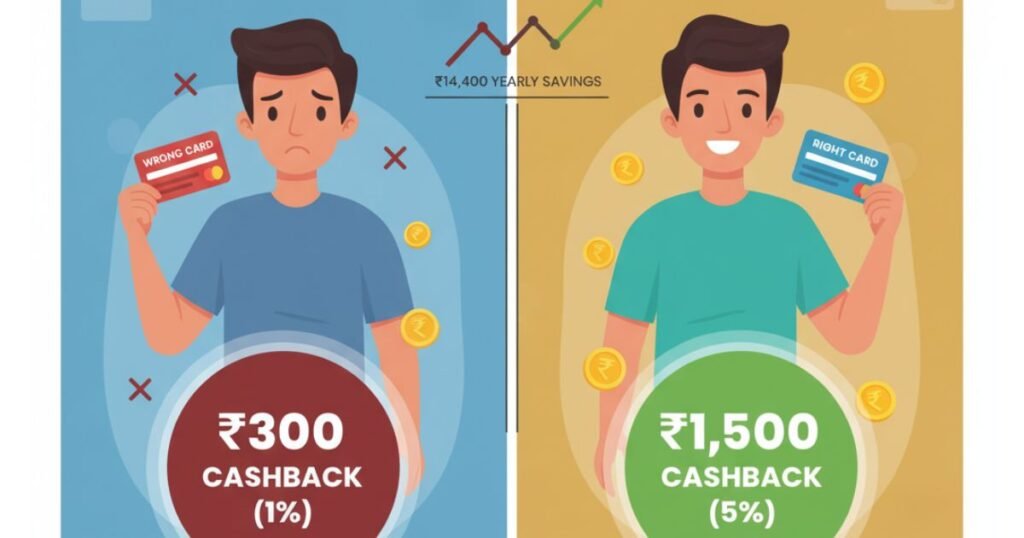

Think about it. If you spend ₹30,000 a month online.

- The WRONG Card gives you 1% cashback. You save ₹300.

- The RIGHT Card gives you 5% cashback. You save ₹1,500.

That’s a difference of ₹1,200 every month, or ₹14,400 every year

You are leaving real money on the table by using the wrong card. This article will help you find the right card for your spending.

How to Pick Your Perfect Card

Here is the simple, 3-step way to choose.

Step 1: Find Your Biggest Spend

First, look at your bank statement. Where does 80% of your money go?

For most salaried professionals in India, the list looks like this

- Online Shopping (Amazon, Flipkart, Myntra)

- Food & Groceries (Swiggy, Zomato, BigBasket)

- Utility Bills (Phone, Electricity, Gas via Google Pay, etc.)

- Fuel (Petrol/Diesel)

Your goal is to find a card that gives 5% or more on these categories.

Step 2: The 3 Best Cards for Online Shoppers

Based on our research, these 3 cards are the best for the 80% of people who spend online.

- Cashback SBI Card

This is the king of online cashback. Why? It’s simple. It gives 5% cashback on all online spending SBI Cashback Credit Card. It doesn’t matter if you shop at Amazon, Flipkart, Myntra, or any small website. You get 5% back.

- HDFC Millennia Credit Card

This is another amazing card. It gives 5% cashback on a list of popular websites, including Amazon, Flipkart, Swiggy, and Zomato HDFC Millennia Credit Card If you spend most of your money on these specific apps, this card is perfect for you.

- Axis Bank ACE Credit Card

This card is a champion for bill payments. It gives 5% cashback on all bill and recharge payments you make through Google Pay. It also gives 4% on Swiggy, Zomato, and Ola Axis Bank ACE Credit Card If bills are your biggest expense, this is your card.

Step 3: A Simple Comparison

Here is a simple table to help you decide.

| Card Name | Best For (The 80/20) | Cashback Rate | Annual Fee |

| Cashback SBI Card | All Online Shopping | 5% on any website | ₹999 + GST (Waived if you spend ₹2 Lakhs) [Source 95] |

| HDFC Millennia Card | Popular Apps | 5% on Amazon, Flipkart, Swiggy, etc. | ₹1,000 + GST (Waived if you spend ₹1 Lakh) [Source 7] |

| Axis Bank ACE Card | Utility Bills & Food | 5% on Bills (via GPay), 4% on Swiggy | ₹499 + GST (Waived if you spend ₹2 Lakhs) [Source 39] |

Pros & Cons

Cashback cards are great, but you must be careful.

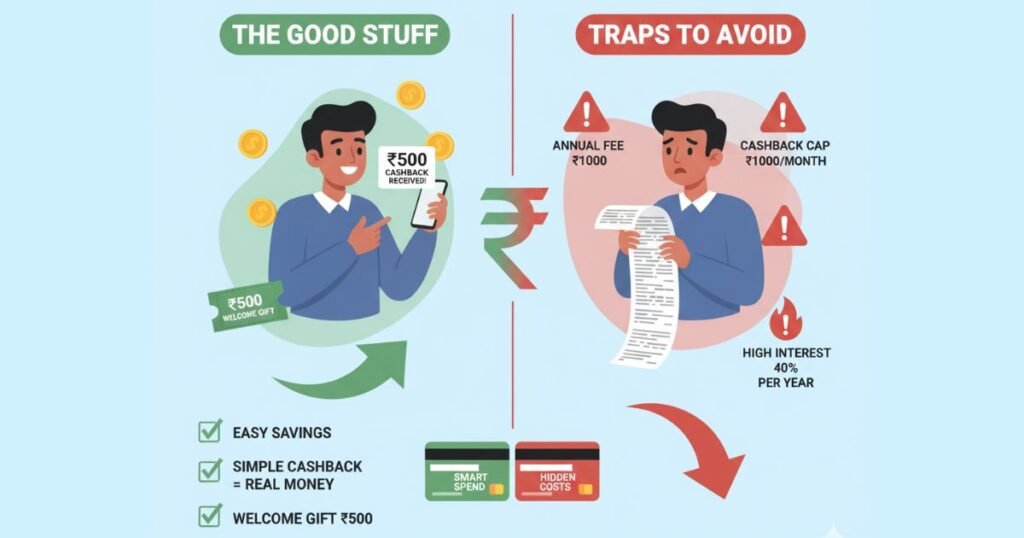

The Good Stuff

- Easy Savings: You save money without doing any work.

- Simple to Understand: Unlike reward points, cashback is just money. ₹1 cashback = ₹1.

- Good Welcome Gifts: Many cards give you a ₹500 voucher when you join.

The Traps to Avoid

- Annual Fees: Many cards have a fee (like ₹500 or ₹1,000) every year. You must spend enough to save more than the fee.

- Cashback Caps: This is the most important trap. A card might say 5% cashback, but have a cap of only ₹1,000 per month. This means after you spend ₹20,000, your cashback stops.

- Interest Charges: NEVER pay just the minimum due. If you don’t pay your full bill, the bank will charge you a very high interest (sometimes 40% per year). Pay your bill in full, every single time.

Expert Quote Box

“A credit card is a tool. Used wisely, it builds your wealth. Used poorly, it builds your debt. The minimum due payment is the most expensive trap in finance. Always pay 100% of your bill.”

– Shovit Goyal

How to Apply

You can apply for these cards online.

Frequently Asked Questions

Q: What is an annual fee?

A: This is a small fee the bank charges you every year to use the card. Most banks will waive (cancel) this fee if you spend a certain amount of money in the year.

Q: What is a cashback cap?

A: This is the maximum amount of cashback you can earn in a month. For example, the HDFC Millennia card has a cap of ₹1,000 per month.

Q: Is a co-branded card (like Flipkart or Swiggy) a good idea?

A: Sometimes. The Swiggy HDFC Card gives 10% cashback on Swiggy. If you order from Swiggy every day, it’s a great card. But if you also shop on Amazon, the Cashback SBI card is better because it works everywhere.

Q: How many credit cards should I have?

A: Start with one good card that matches your main spending. After 6-12 months, you can get a second card to cover another category (like a fuel card to use only at petrol pumps).

About the Author

Shovit Goyal is a Financial Content Creator with 6 years of experience in the financial services industry. He is passionate about teaching financial literacy to young professionals across India. His goal is to help people stop being afraid of finance and start using it to build a better future. He believes that the right financial knowledge can turn anyone’s salary into real wealth.

You can connect with him on : Linkedin

Disclaimer:

The information in this article is for educational purposes only and is based on data available as of October 2025 from bank websites and public data. It is not financial advice. All credit card offers, fees, and cashback rules can change. Please read the card’s official documents carefully before applying. Shivanshi Enterprises is not responsible for any decision made based on this content. We may earn a commission from affiliate links at no extra cost to you, which helps us create this free content.